The Power of Life Insurance & Annuities in Retirement and Beyond

RECEIVE A $10 MILLION RETURN FOR A $75 THOUSAND ANNUAL OUTLAY

If you are making some of your investments in order to provide a greater legacy

to your heirs, you need to be acutely aware of the fact that each and every dollar

you leave them in excess of your combined spousal exemptions will be subject to

estate taxes of up to 55%. That means that if your investments have a total value

of $20 million at the time of your death, your heirs will only receive approximately

$10 million. Right away, the day you die, your investments have become devalued

by 50%.

Life insurance is THE ONLY financial vehicle which can provide a means to retain

your assets' full value to your heirs.

And there is a way that you can utilize the already existing power of your current

investments to borrow the cost of the insurance so that you can earn a return equal

to the full $10 million which would otherwise be lost to taxes for only $75,000

a year!

If you and your wife are average age sixty and in reasonably good health, there

is every reason to believe that you can receive a 10-to-1 return on your insurance

dollar. That means that it would cost you $1 million to replace the $10 million

that will be lost to taxes at your deaths. This is a substantial return yet it is

an even more incredible when you consider the fact that it will be available to

your heirs the very day the insurance purchase is completed and will not be subject

to the 50% decimation of estate taxes if structured correctly.

It would seem that an outlay of 1/20th of your total estate valuation - 5% of your

total asset -- would be well worth it in order to protect $10 million of your heirs'

legacy. Furthermore, in real dollars, that $1 million outlay only costs $500,000

since it too would have been halved by taxes had it been left inside your estate.

But you need not expend even this much in order to achieve the desired result. In

fact, you can provide your heirs with the entire $10 million for an outlay of approximately

$75,000 a year!

With an estate valued at $20 million, assuming current LIBOR or broker call rates

of 7 1/2% interest, you could easily borrow the $1 million cost needed to execute

the Investment Alternative concept for $75,000 a year.

In this way, only $75,000 a year provides a return of $10 million, based on the

current assumptions at the outset.

Supposing you were to live to be 80. You would wind up paying the $75,000 interest

for 20 years and the total cost would only be $1.5 million. But remember, if you

did not pay that $1.5 million in interest for the insurance policy it would have

remained within your estate and been subjected to the same 50% estate taxes that

the rest of your estate will be assessed. So, to your heirs, that $1.5 million was

only worth $750,000. In effect, you actually purchased the $10 million for an accumulated

net cost of $750,000. That becomes equivalent to a more than 13 times return.

Even if you could do something else with that $1.5 million that would eventually

yield the same $10 million any investment return you are fortunate enough to earn

will be subjected to the same 50% taxes upon your death. A $1.5 million investment

must increase to $20 million from the time you are 80 before you die, in order to

be worth the same $10 million to you heirs.

When you die, your heirs will have to repay the $1 million loan amount from the

$10 million they inherited from you. But, even if you lived to be 80 and paid $1.5

million in loan payments in addition to the $1 million loan amount itself, the total

cost would still only be $2.5 million. But consider this: The outstanding $1 million

loan is a liability against your estate. This means that your estate is no longer

valued at $10 million; the $1 million outstanding loan amount has reduced its value

to $9 million. The estate taxes due on $9 million are not $5 million, but $4.5 million.

Your net estate tax has been reduced from $5 million to $4.5 million! A difference

of only $500,000, not $1 million.

In effect, Uncle Sam repays 1/2 your loan and loan interest!

AVOID THE GUARANTEED 4500 POINT STOCK MARKET CRASH

Chances are that your portfolio carries a number of investments that are traded

on Wall Street all of which were purchased as hopeful growth assets. You've no doubt

consulted with your advisors, set out the goals you desire your investments to achieve

and selected the vehicles which you all agree are most likely to accomplish those

goals. Though you are aware that there's a risk involved in investing, it's a calculated

risk deemed appropriate to the expected, potential rewards.

So the days go by, and the market fluctuates within tolerable limits, some days

up, some days down, and you watch your investments and make adjustments where it

seems necessary and feel safe that it is all well within projected parameters.

Then, one day, out of blue, completely unexpectedly, the stock market crashes 4500

points and all your investments are devalued by as much as 55%!

Sounds ridiculous? It isn't. That day is coming as sure and certainly as the sun

will rise tomorrow.

As far as you and your investments are concerned, the market will crash 4500 points

the day you die.

Nine months after you die, up to 55% of your net worth will be assessed in estate

taxes. Suppose you and your spouse, together averaging age 70, had $3 million in

investments above and beyond whatever other assets you have and need to maintain

your lifestyle. As part of your total estate, the $3 million is subject to 55% estate

taxes that will be assessed on your net value. That means it will really only be

worth $1.3 million to your heirs. The market will crash and the investments you'd

earmarked for your children's financial security will crash along with it.

There is a way around this devastation.

If you had taken a small portion of the funds you'd invested, $330,000 from the

$3 million, and diversified your portfolio with life insurance, you could, even

at age 70, receive a 5 - 1 return, based upon current assumptions. Your $330,000

outlay would produce $1.6 million to replace what was lost in the estate tax "crash."

This might be the best "hedge" you have ever made.

This strategy does not involve any other expenditure of money than you were already

making. It simply required that you diversify your investments and move some of

the funds already earmarked for growth for the good of your children into the purchase

of an insurance policy that, by virtue of its unique financial attributes, is able

to protect all the rest.

If there are principal assets included in your net that you do not need in order

to preserve your lifestyle, there is no better diversification you can make then

the one which protects all the others.

Figure out how much you will lose when the market crashes for you: take your investment

totals and, for the sake of simplicity, divide them in half. Now, based on your

age, divide that number either by 10, 5 or 3. This will give you the amount, appropriate

to your age that you would need to divert and diversify from your existing in order

to replace the half lost to estate taxes for your heirs. Look at the numbers, and

remember that any investment you might consider utilizing to replenish the tax drain

must actually increase in value 200% in order to yield, after taxes, the same 100%

recovery that this approach inherently provides.

INCREASE YOUR IRA OR PENSION UP TO 20 TIMES, TAX FREE

If you don't need the income from your IRA or Pension Fund to support your lifestyle

and provide for your retirement, you may be wasting a great deal of money.

Whatever tax advantages your IRA or Pension provides during your lifetime, all assets

contained within them at the time of your death will still be subject to income

taxes and up to 55% estate taxes that will ravage your heirs' inheritance.

This means that if you have an IRA or Pension fund worth $2 million and are worth

more than $3 million in total, income taxes of approximately $800,000 and estate

taxes of $660,000 will reduce its value to only $540,000 to your heirs.

But if you terminate the IRA or Pension now you can greatly increase your legacy.

After paying income tax of approximately $800,000 upon the termination of your fund,

you will be left with $1.2 million. By using that $1.2 million to purchase a last-to-die

life insurance policy on you and your spouse you can receive an up to 10 times return,

based on your age and current assumptions. Your heirs can receive $12 million instead

of $540,000. Furthermore, the $12 million will come to your heirs income and estate

tax free.

Your $2 million IRA or Pension would have to increase over 22 times to become worth

$45 million in order to produce the same after-tax $12 million for your children.

A $45 million IRA would be subject to about 40% income tax of $18 million. The remaining

$27 million would then be subject to 55% estate tax of $15 million leaving $12 million.

Do you really believe your $2 million IRA or Pension is going to increase to $45

million? Do you have any guarantee that it will do so in the time you have left?

Of course not, since you can not know how much time that is.

At age 70, your $1.2 million can produce up to $6 million and even at age 80 you

can optimize it up to $3.6 million.

Clearly, this program out performs your IRA or Pension at virtually any age if you

don't need the income to provide for your own well-being.

What is the point of retaining your IRA or Pension for your heirs when Wilson Financial

life insurance method can perform so much more effectively? The answer -- there

is none.

INCREASE YOUR ANNUITIES 10 TO 20 TIMES, TAX FREE

There are currently over $1 trillion worth of annuities in force in the marketplace.

Bought to accumulate money on a tax free basis, they were an excellent selection

when first purchased.

But for many families the usefulness of annuities has passed, often without their

noticing.

If you're holding annuities for the eventual benefit of your heirs, you should know

that at your death, the annuity will be subject to both income and estate taxes.

Their value to your heirs will be greatly reduced. There is a way to avoid this

tax decimation AND provide an even greater legacy for your heirs.

Assume you purchased an annuity for $100,000 and it has now grown to $300,000. At

your death, income taxes on the $200,000 annuity gain will be $80,000 and estate

taxes will be $120,000 leaving your heirs only $100,000 -- exactly what you started

with.

But, if you take a distribution of the annuity now and pay the income tax of $80,000

you will still have $220,000 left. Used to purchase a one-pay, last-to-die life

insurance policy, that $220,000 could produce $2.2 million if you and your spouse

are age 60; $1.1 million if you're age 70; and $660,000 at age 80, based on current

assumptions.

Clearly, there is no better way to optimize your annuity and uphold your objective

of providing an enhanced legacy for your heirs.

Why would you hold an annuity that is going to be reduced to its original value

with no gain to be shown for all the years you held it when you could use simple

principles of diversification to provide up to 20 times more?

OPTIMIZE MUNICIPAL BOND YIELDS UP TO 25% YEARLY

Do you have significant assets in Municipal Bonds to take advantage of their tax

free nature? If so, you may want to reconsider because Municipal Bonds ARE NOT tax

free. They are income tax free, and that's good. But they are NOT estate tax free.

Yes, municipal bonds can save you the up to 40% tax assessed on the income they

generate. But they will do nothing to avoid the up to 55% estate tax your assets

will face at the time of your death.

Maybe you don't even need the 40% tax savings to afford your lifestyle and are using

it to grow your estate for your heirs. But it will still be halved by estate taxes.

Even more confusing, maybe you DO need the extra income. Then what do you do to

provide for yourself AND provide for your heirs?

Here's what.

To illustrate this program, let's assume you are 75 years old and have an estate

worth $50 million of which $10 million is currently invested in municipal bonds.

The bonds yield about 5% a year, which is $500,000. Because of the muni bonds' tax

free nature, you -save' $200,000 a year in income taxes.

However, at the time of your death, your bonds will be subject to estate taxes of

$5 million. It would take 25 years of savings at the rate of $200,000 per year to

equal that pending $5 million loss. But, to make up for the estate tax loss, it

would take 50 years because those savings, as part of your estate, are ALSO going

to be halved by estate taxes. Those municipal bonds aren't looking quite so good

anymore are they?

There is a way to retain the full income your bonds are currently providing AND

protect your asset's full value for your heirs.

Using an Immediate Annuity, for the same $10 million at average age 75, you and

your spouse could receive an annual income of approximately $1 million AFTER TAX

based on current assumptions. If you kept for yourself the same $500,000 that your

municipal bonds are currently yielding, you would have an extra $500,000 a year

in income. Even at age 75, you can use that annual $500,000 to purchase a last-to-die

life insurance policy that will produce up to $14 million for your heirs. The $14

million will be income tax free and, as long as it is properly structured in an

Irrevocable Trust, estate tax free as well.

You retain the full income you are used to and your heirs receive $14 million instead

of the $5 million they would have gotten after the $10 million of municipal bonds

was halved by estate taxes.

And the best news of all is that this plan works BETTER the older you are.

A female age 85 would receive annual income of $1.77 million from the same $10 million

outlay. This is not a trick or some complicated machination. It is simple, bottom

line mathematics creatively applied. It's irrefutable, inarguable and simply the

single best method for optimizing your assets.

TURN A $10 THOUSAND TAX FREE GIFT INTO A $1 MILLION GIFT AT NO EXTRA COST!

Tax laws allow each of us to gift everyone we want up to $10,000 per year without

having to pay any gift or transfer tax. By making these gifts, you are removing

the money from your estate on a tax free basis; what you don't give away each year

while you're alive will become automatically devalued by as much as 55% upon your

death.

If you were to take the annual $10,000 you intend to gift your child and, instead

of giving it to him or her directly, were to place it in an Irrevocable Trust and

have the Trust use it to purchase a life insurance policy on you and your spouse's

lives, your child would receive a 3, 5 or even 10 times return at the time of your

death. This could result in your annual $10,000 gift becoming worth as much as $1

million to your heirs, all of it income, estate and gift tax free.

If your financial situation permits, you and your spouse can take further advantage

of tax law by each gifting $10,000 annually and using the combined $20,000 to produce

up to $2 million for your heirs. That is a 100 times increase over the annual $20,000

gift in any given year!

You can utilize and combine these potentials to customize a solution to virtually

any situation.

If your children need some financial help now but you still want to optimize your

giving, one of you could make a direct gift of $10,000 for their immediate benefit

while the other used their $10,000 to fund the insurance to still produce up to

an additional $1 million. That would be $10,000 a year direct to your child and

another $1 million upon your death. Clearly, in this example, there is simply no

investment you can name which can realize these achievements.

Even if you have to pay gift taxes of $5,000 to give away an additional $10,000,

this program still works to fully optimize your funds like no investment can.

Let's assume that you have already made the maximum allowable tax free gifts to

your children and do not want to pay gift taxes but would still like to help them

further. You can still maximize an extra $10,000 gift more than 50 times. Simply

earmark an additional $7,000 for your child. You will pay gift taxes of approximately

$3,000. But if you don't make that gift that same annual $10,000, sitting within

your estate, will be reduced by 55% upon your death to less than $5,000.

Of course, if you are willing to pay the gift taxes - and there's no reason you

shouldn't be since, in the end, you will still be saving estate tax costs and greatly

optimizing your gift - there is no need to restrict the amount of your gift to $10,000.

You could apply this program to any sum available for you to gift without negatively

impacting your own lifestyle. And remember, in addition to annual $10,000 gifts,

both you and your spouse are permitted under federal tax law to gift anyone of your

choosing with one lifetime gift of $600,000, the amount of the one-time estate tax

exemption you are probably familiar with. You can apply the same $7,000/$3,000 gifting

techniques to your $600,000 one time exemption by giving $400,000 to whoever you

want and paying $200,000 in gift taxes.

You can have as many $600,000 exemptions as you want as long as you don't use more

than 2/3's of each one as a gift.

If you can afford to do so, rather than passing $600,000 to your heirs tax free

at your death, consider gifting it to them now. You still will not pay any estate

or gift or transfer taxes -- your exemption is available during your lifetime as

well as at your death - but you will be able to greatly increase and optimize the

gift through the shrewd usage of a one-pay, last-to-die insurance taken out on you

and your spouse. $600,000 applied to this program would net a return for your children

of up to $6 million! You could even go one step further and utilize both $600,000

exemptions to which you and your spouse are entitled for a combined investment total

of $1.2 million. Utilized in the same way to purchase a last-to-die insurance policy,

that $1.2 million will be worth $12 million to your heirs income and estate tax

free.

What stock, bond, T-Bill, piece of property or other conventional investment will

increase from $1.2 million to $12 million during the remainder of your lifetime?

More on point, what stock will increase from $1.2 million to $24 million in order

to equal the same $12 million for your heirs after estate taxes are assessed?

You can also use this program to increase your income to your spouse up to 6 times

upon your death.

$600,000, passed to your spouse at your death, will produce, annually, approximately

$30,000 income assuming a 5% interest rate.

By placing the $600,000 into an Irrevocable Trust and using it to purchase a life

insurance policy on yourself for his/her benefit, at death your $600,000 exemption

could be worth as much as $3.6 million, depending on your age and health at the

time the life insurance policy is purchased. The trust is structured so the spouse

can have the income during his/her lifetime while the principal remains for the

heirs. $3.6 million will produce $180,000 annually at the same assumed 5% interest

rate. In this manner you have increased your spouse's income from $30,000 to $180,000

a year, every year, for the rest of your spouse's life without paying a single additional

dime of tax.

PUT YOUR YOUTH TO WORK EARNING AMAZING RESULTS

As phenomenal as the applications for life insurance in estate planning are for

people in their sixties, seventies and eighties, they can be even better for young

people in their thirties, forties and fifties. And though it has not historically

been common for people at those ages to think in terms of life insurance purchases,

doing so can open the door on incredible opportunities for wealth creation and optimization.

A last-to-die life insurance policy bought on a one-pay basis can provide a 10-to-1

return at age 60, based on current assumptions. The same policy, if bought at age

50, can yield a 16-to-1 return. At age 40 the return can be 28-to-1 and at age 30

the policy can produce an incredible 50-to-1 return.

Furthermore, as with all insurance policies the benefits are income tax free and,

if structured properly in an Irrevocable Trust, estate tax free as well.

Any other use of the same money would have to yield returns almost four times as

high in order to net the same after income tax of 40% and estate taxes of 55%.

It would require that your $20,000 grow to almost $4 million so that after income

taxes of $1.6 million and estate taxes of $1.3 million it would equal the same $1

million the insurance will provide. Yet, you have no promise of equal or greater

returns through any other financial vehicle and you have no guarantee that you will

live the full lifetime needed to achieve them if they do exist. Prudence requires

you diversify your portfolio to include life insurance.

You can use the insurance to create incredible principal for your children at greatly

discounted rates. Imagine the legacy you can begin creating using these tremendous

returns. Your dreams of financial security and well-being for your heirs can be

realized for as little as 2 cents on the dollar.

You can also use life insurance to provide a perpetuity of income for your heirs

by naming a trust as the beneficiary of the insurance. At your deaths, the trust

receives the insurance benefits. It can then hold the principal and disperse the

income it generates. Assuming interest rates of 5%, a $1 million death benefit would

earn $50,000 a year. Your trust can pay this $50,000 to your heirs and then, later,

to their heirs, creating an estate-tax free family dynasty. Structured properly,

the Trustees can then disburse the principal at any time should changes in interest

rates or family economic needs make this a prudent thing to do.

Another way to take advantage of the incredible returns available at young ages

is as the ultimate gift from grandparent to grandchild.

A 10-to-1 return at average age 60 is a very valuable thing. But if the 60-year-old

couple really wants to maximize the funds they have available, they might want to

consider purchasing a policy on their children for the sake of their grandchildren.

Now the return jumps from 10-to-1 to up to 50-to-1 making every dollar spent worth

$5 more than it otherwise would have been and this can be done with tax deductible

borrowed money.

Lastly, this program is an especially wonderful way for parents to use their children

to make truly significant gifts to charity.

If your children were average age 40 and you were in a position to make a $100,000

gift to charity, the charity you selected would be grateful to accept your generosity.

However, think how much more good works $2.8 million could do. That's how much you

COULD be gifting if you used the $100,000 to buy a last-to-day life insurance policy,

based on current assumptions, and named the charity as beneficiary. Yes, the charity

would have to wait a longer period of time before receiving the funds, but there

will always be good works that need to be done and $2.8 million will help a lot

more people than $100,000. This is charitable giving at its absolute most optimized

best.

Clearly, the applications of life insurance for wealth creation are unparalleled

at younger ages. Yet many people do not consider a life insurance purchase until

they are older. Don't be one of those people. Don't miss out on the best returns

you will almost assuredly ever encounter and the best, most sure chance for true

financial optimization.

CREATE MONEY VIRTUALLY OUT OF THIN AIR

The concerns of wealth creation and preservation are not limited to the young. In

fact, it is generally at older ages that these concerns really present themselves.

For many of us, after a certain age our earning potentials plateau and dip. In most

cases, one of the things we focus on most is what legacy we will have to leave our

children. But, at the same time, our need for expanded sources of income may grow

as medical bills increase or simply because we now desire to enjoy some of the things

we wanted to do before but didn't have the time or resources for.

It is difficult to balance these two seemingly conflicting desires: wanting to have

more for ourselves and wanting to leave more for our heirs. Few financial vehicles

can accomplish both goals. But one can.

One financial vehicle is available to people of older ages that can allow them to

virtually pull money out of thin air without capital gains taxes, very little income

taxes, with no loss of current income, no loss of future appreciation of their gross

stock portfolio and no cash flow impairment AND, at the same time, provide for their

heirs' well being without any gift or estate tax.

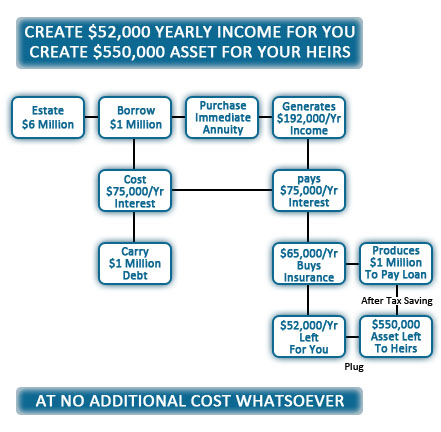

A man age 85, has an estate worth $6 million almost all of which is held in stocks

and bonds. Taking advantage of the margin available through his stock brokerage

firm, he borrows $1 million against those assets. By doing so, he pays no capital

gains taxes on the newfound money, nor does it diminish his cash flow at this time.

All assets are intact and in place to continue earning the same dividends or returns;

all future growth potentials remain undisturbed.

The man takes the $1 million and uses it to purchase an immediate annuity which

guarantees him an income for as long as he remains alive. Right away new income

has been created from nowhere.

The income generated by the $1 million annuity is $192,00 per year after tax, based

on his life expectancy. From that, he pays the $75,000 thousand which is due on

the margin loan from his stockbroker which leaves $117,000 annually. From that annual

$117,000, he takes $65,000 each year for the purchase of a life insurance policy

which will yield, at his death, $1 million for his heirs to use to pay off the $1

million principal from the loan from the stock brokerage firm. The man pays no gift

tax on the transfer of the money and the heirs pay no income or estate tax on its

receipt. Not a single dime of the children's inheritance is impacted and yet an

extra $52,000 annually has been created for the man to enjoy spending every year,

even after paying the loan interest and even after purchasing the insurance policy.

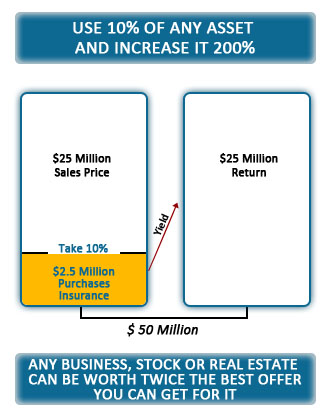

DOUBLE THE SALE PRICE OF YOUR BUSINESS OR REAL ESTATE

How would you like to double the sale price you receive for virtually any item of

value you possess? You can. And more than that, you can effectively triple the price

your heirs receive for it.

Let's assume you own a business that you have built and developed and run for years

and years. Now, it's time to get out; you put the business up for sale. Finally

the sale is consummated and you have received $25 million.

You can now, after the sale is accomplished, double the sale price received for

the asset.

Assuming that you and your spouse are age 60, you can take 10% of the proceeds from

the sale of your business -- $2.5 million -- and use it to purchase a life insurance

policy that will yield, based on current assumptions, $25 million. This simple reallocation

of a portion of your asset will basically double the amount the business sale netted

from $25 million to $50 million.

Yes, that $50 million is actually reduced to $47.5 million by the outlay of the

$2.5 which funded the additional $25 million death benefit. And yes, there would

be some gift taxes to pay on the transfer of the $2.5 million from your estate to

the Irrevocable Trust on behalf of your children. However, you and your spouse are

together entitled to a one-time gift and transfer exemption so taxes will only be

assessed on what remains after that. At approximately 40%, that gift tax would be

about $500,000 depending on the year in which this transaction occurred and the

transfer exemption current at that time. So, in fact, the $50 million would be reduced

$2.5 million by the cost of the program and $500,000 in gift taxes. Now, instead

of $25 million from the sale, you 'only' receive $47 million. Is that close enough

to double not to quibble?

Meanwhile, when the original $25 million from the sale of the business came to your

heirs, it would have been reduced by estate taxes of 55% to $11.25 million. If you

undertake this program, that amount will be somewhat further reduced by the $2.5

million of the insurance purchase cost and the $500,000 of gift taxes. The $25 million

will become $22 million, which will be subject to $12 million in estate taxes leaving

$10 million. So it might seem that your heirs have 'lost' 1.25 million. But with

the additional, tax free $25 million which your heirs will receive from the insurance,

the total value of the asset to them has jumped to $35 million and that's still

over three times the net $11.25 million they would have received had you not undertaken

the program.

You could borrow the $2.5 million insurance premium instead of paying cash from

the newly sold asset and either pay the approximately 7% interest of $175,000 each

year or you could borrow it and let the interest accrue. In either case, you would

not lose the use of the additional 10% of your asset and the total net cost of the

loan, whether paid or accrued, would still be well worth the return of $25 million.

The same concept applies to increasing the value of any real estate or stock that

did not perform as well as you had wished for.

Your real estate is sold for $3 million. You pay capital gains tax of approximately

$1 million leaving a net gain of $2 million. You ultimately die and your heirs pay

approximately $1 million in estate taxes leaving a net value for your real estate

sale of $1 million. Following this plan, you would have used $300,000 (10% of $3

million) to purchase a last-to-die insurance policy with a return of $3 million

(age 60), $1.5 million (age 70), or $1 million (age 79). In every case you have

increased the net value of the sale of your real estate from $1 million net to $2

million, $2.5 million, or $4 million, from two to four times what your heirs would

have received had you done nothing.

This same technique also applies with the sale of any other asset.

Since this money would not have been received by your heirs before the event of

your death, for all practical purposes you can consider that you sold the business,

real estate, or asset for double to quadruple its net sale value. Frankly, your

children, grandchildren, other heirs or charity will not care whether the $2 to

$4 million came from the asset sale or a combination of the sale and insurance.

These techniques can also be used to help you achieve a desired sale price that

you couldn't receive instead of just maximizing a sale.

Let's say you felt your business was worth $25 million but you could only get $20

million for it. Now you are faced with a $5 million 'loss' of your business' expected

value and you might be tempted to turn the $20 million offer down and wait and hope

someone comes along and offers the full $25 million. You could wind up waiting a

long time.

Or, you could take the offered $20 million and use life insurance to create the

'lost' $5 million or more.

With the 10 times return on an insurance purchase you are earning at your average

ages of 60, you and your spouse could take $500,000 of the proceeds from the sale

of the business and purchase a one-pay, last-to-die policy that would yield at death,

$5 million income and estate tax free. For ten cents on the dollar you have recaptured

the $5 million and sold the business effectively for the full $25 million you desired.

You could use $1 million and buy $10 million thus raising the value of the sale

from $20 million to $30 million, $5 million more than you originally wanted. In

fact, you could double the value of the sale from $20 million to $40 million by

using $2 million to buy the insurance.

You can apply this technique to the sale of any asset for which you can not now,

and may not ever, receive what you desire or think it to be worth so that your heirs

will benefit from the full value of the business, property or other asset you have

spent a lifetime amassing for them.

GO BACK IN TIME TO EFFECTIVELY BUY MICROSOFT BEFORE IT WENT UP 10 TIMES

It's a common theme in science fiction stories. Someone gets hold of a time machine

and uses it to travel backwards through time. Then, using his future knowledge of

the outcome of current events, the time traveller is able to take advantage of financial

opportunities that he knows will increase in value tremendously once he's back in

his own time.

Wouldn't it be great if you could really travel back in time to take advantage of

the opportunities you passed up that are now so valuable? Using Wilson Financial

remarkable techniques, you can.

Imagine getting in on Microsoft, Starbucks or Netscape before they went through

the roof.

To illustrate this program, suppose there was a stock that was selling for $10 a

share a few years ago. You turned it down and now it's selling for about $200 a

share and you're kicking yourself. Hard. Had you invested $100,000 in the stock

when the chance was first offered, you would have bought 1,000 shares. Now those

shares would be worth $2 million before estates taxes and about $1 million after

taxes.

If you are worth more than $3 million and have some other stocks in your portfolio,

you could sell $100,000 worth and use the money to buy a $1 million last-to-die,

one-pay life insurance policy, based on current assumptions. Assuming you and your

spouse average age 60, your $100,000 diversification from your stocks to the life

insurance policy will provide a return of the entire $1 million after-tax value

of the missed stock opportunity.

The same $100,000 that you didn't invest then and now regret, can fund the exact

same return.

Take your life insurance policy and put it in a file labeled Microsoft. At your

death, your heirs may be surprised to discover that you weren't a stock-picking

genius, but they'll be glad you were smart enough to recapture the opportunity the

best way there is.

GIVE AWAY YOUR FULL ESTATE VALUE TWICE WITHOUT PAYING ANY ESTATE TAXES

The purpose of estate planning is to arrange your assets in such a way as to maximize

the amounts of money you leave your heirs and minimize the amount of taxes you pay

in the process. Without planning of this sort estate taxes, which can reach as high

as 55%, devalue your estate and dramatically reduce the inheritance you leave behind

for your heirs.

Only life insurance in an Irrevocable Trust can actually create money where none

was before, replace tax losses and recreate the wealth that would otherwise be gone

for good.

There are only two ways to avoid all estate taxes on any sum of money beyond the

combined exemptions allowed to you and your spouse. One is to remove the entire

sum from your estate prior to your death in which case you will pay gift taxes that

are almost as decimating as estate taxes. The other is to leave the entire sum to

charity.

However, there is a way to leave everything you have to charity and therefore pay

no estate taxes while still also leaving the entire current value of your estate

to your heirs and paying no estate taxes.

It's simple, it's legal, and it absolutely works.

Let's say you and your spouse are average age 60 and have an estate worth $8 million.

If you do nothing, estate taxes will claim about $4 million leaving your heirs $4

million. But, if you follow this plan, you can leave your heirs the entire $8 million

while at the same time leaving $7.2 million to charity and all without a single

dime of estate tax liability.

It works like this: At average age sixty, you and your spouse can expect to receive

a 10 - 1 return, based on current assumptions, on a last-to-die life insurance policy.

You transfer $800,000 to an Irrevocable Trust which uses the funds to purchase a

last-to-die policy on your lives and, since the $800,000 is less than your combined

marital gift and transfer exemptions, you would pay no gift tax on this transfer.

At your deaths, the insurance policy will return a death benefit of $8 million to

your heirs. Because of the unique nature of life insurance proceeds, the death benefit

will come to your heirs income tax free. And because the policy was held in an Irrevocable

Trust outside your estate, they will not have to pay any estate taxes on it either.

After making the one-time expenditure of $800,000, your estate was reduced from

$8 million to $7.2 million. For the rest of your lives, you have the use of this

principal and the income it produces to support your lifestyle. Then, when you die,

you leave the entire sum to charity and, in so doing, avoid all estate taxes on

the total asset. The charity gets a tax free $7.2 million while your heirs get a

tax free $8 million all from the same original $8 million.

You have accomplished both goals of estate planning. You have maximized the legacy

your children receive and you have completely eliminated all estate taxes. You have

given your entire estate away to charity. And you have left your entire estate to

your heirs. And not a single dime of your asset was lost to taxes.

DISCOUNT YOUR ESTATE TAX COST UP TO 90%

Estate taxes are a reality with which we all must live and die. Recent changes in

the tax code do impact estate taxes, but they don't negate them.

The fact remains that if your estate is worth $3 million or more your heirs will

be faced with up to 55% estate taxes.

But it doesn't have to be this way. Using Wilson Financial techniques, you can effectively

pay your total estate tax at up to a 90% discount.

Let's assume that you and your spouse are average age 60 with an estate worth $30

million. This program will work at all ages and for any estate over $3 million.

To figure out how it applies to you, just pro rata all the numbers up or down.

The 55% tax on your $30 million estate will be $16.5 million leaving your heirs

$13.5 million. At average age 60 you can receive a 10-to-1 return on the purchase

of a last-to-die insurance policy, based on current assumptions. This means that

for a $1.65 million single payment, you can buy a life insurance policy that will

yield $16.5 million to your heirs. These proceeds can come to your heirs income

and estate tax free.

Of course, if you prefer, you can always buy the policy on a limited-pay or life-pay

basis as well which will increase your total cost but greatly reduce your initial

outlay. There are even ways to purchase the insurance without any outlay during

your lifetime. But however you initiate the program, the bottom line remains the

same. By using life insurance, you provide the funds for your heirs to pay the estate

taxes for as little as only 10 cents on the dollar.

This is estate tax cost discounting at its simplest and most effective.

INCREASE CHARITABLE GIVING MANY TIMES OVER AT NO ADDITIONAL COST

Charitable giving is a great tradition in America. Yet, while many people give all

they can and wish they could give more, not enough are taking advantage of the one

best means to maximize every dollar donated.

Life insurance is tax deductible if you have as its stated beneficiary a charity

or foundation.

If it is your intention to gift some portion of your estate to charity, there is

no better way to do so than to use life insurance to completely maximize the gift

at no additional cost to you or your heirs.

Use the amount you have slated for charity to buy a last-to-die insurance policy

on the lives of you and your spouse. Based on current assumptions, your charity

can receive a ten times return if you are average age 60, five times if you are

70 and three times if you are 80. That means that a $100,000 gift becomes worth

$1 million, $500,000 or $300,000.

To maximize the gift even further, buy the policy on the lives of your children.

At younger ages the return can be as high as 50 times turning your $100,000 donation

into $5 million.

Of course, you can use a combination of policies to gift some money immediately

upon your death and more later upon the deaths of your children. This way the charity

gets funds sooner and later, all highly optimized.

Creativity applied to charitable giving creates a wealth of opportunities to do

even more good works at no additional cost to you.

EFFECTIVELY EXEMPT YOUR ENTIRE ESTATE FROM ESTATE TAXES

When you undertake your estate planning, you don't need to make any special plans

to shelter the amounts of your individual and/or combined exemptions. These funds

are "exempt" from estate taxation and come to your heirs free from any

estate tax loss.

Well then, if you could effectively exempt your entire estate from estate taxes

wouldn't your planning be much more simple and straightforward? Write down how much

your estate is worth, subtract the amount that is exempt from tax costs - in this

case, ALL of it - and that leaves nothing over which you must agonize and plan.

There is a way to effectively do exactly that.

The power of life insurance in estate tax planning is so great that it can virtually

transform your 1997 $600,000 exemption into a $12 million exemption and your $1.2

million combined exemptions into an astonishing $24 million exemption! That means

you could have no estate tax loss on the first $24 million of your estate.

If you and your spouse are average age 60, you can receive a 10 - 1 return on your

insurance purchase. Therefore, a single $600,000 exemption could be transferred

to an Irrevocable Trust, there would be no gift taxes to be paid as this one-time

$600,000 transfer is exempt, and the trust could use it to purchase a one-pay, last-to-die

policy on the lives of both of you. That policy would yield $6 million, based on

current assumptions, for your heirs income and estate tax free and $6 million will

cover all estate taxes on an estate of about $12 million. You will have effectively

exempted $12 million of your estate from suffering any loss due to estate taxes.

Your original $12 million of assets passes to your heirs virtually unreduced by

estate taxes since the insurance proceeds pay the necessary $6 million in taxes.

The same plan, if implemented utilizing both $600,000 exemptions -- yours and your

spouse's -- can increase the combined $1.2 million exemptions effectively to $24

million!

$1.2 million used by the same 60 year old couple during their lifetimes to purchase

a one-pay, last-to-die insurance policy will produce $12 million in death benefit,

based on current assumptions. $12 million will pay all estate taxes on an estate

of about $24 million. Therefore, using simple arithmetic, the $1.2 million exemption

has been used to effectively exempt an entire $24 million from estate taxes. Instead

of your heirs paying no tax on the first $1.2 million, they effectively will pay

no taxes on the first $24 million.

Of course, you can use this same program to exempt estates even larger than $24

million. However to do so there will be gift taxes to be paid. If, for example,

your estate was worth $50 million and you needed approximately $25 million to pay

the estate taxes, a one-pay, last-to-die policy on you and your spouse if you are

both 60 years old would cost about $2.5 million. In transferring the $2.5 million,

the first $1.2 million would be exempt from gift taxes as long as you had not already

utilized that exemption. The remaining $1.3 million would be a taxable gift and

the tax would be approximately $520,000. Even so, for $2.5 million plus a $520,000

gift tax you would have effectively exempted your entire $50 million estate from

estate taxes.

Nor are you limited to enacting this program using only the amount of your individual

or combined exemptions.

You can 'purchase' further exemptions by paying the gift tax on any amount of premium

amount needed in excess of your allowable $600,000 or combined $1.2 million.

In this way, you can effectively exempt up to the first $363 million of your estate.

The maximum insurance allowable for any one to buy is $200 million. $200 million

pays all the estate taxes on an estate of $363 million. The cost for a policy which

would yield $200 million would be $20 million for a couple of average age 60, based

on current assumptions. Yet you can not transfer $20 million to an Irrevocable Trust

for the purpose of purchasing life insurance without paying gift tax of about $11

million. The $20 million premium can not fairly be considered an expense since it

will fund a return of $200 million. Therefore, the only real expense associated

with this technique is the $11 million gift tax. Meanwhile, if you do not implemented

this program, the $11 million will remain in yourr estate and, at the time the estate

passed to your heirs, it would have been more than halved by estate taxes from $11

million down to $5 million. So, effectively, it is a cost of only $5 million which

provides the entire $200 million which effectively exempts $363 million from estate

taxes.

At combined age 70, the outlay, based on current assumptions, for the maximum allowable

$200 million of insurance would be $40 million. Gift taxes on the $40 million transfer

would be $22 million which, if left in the estate, would be reduced by estate taxes

to $10 million. Now, effectively, $10 million has provided the $200 million that

exempts the $363 million estate and makes any further estate planning, legal maneuvering

or documents unnecessary.

Even at average age 80, this method works to effectively exempt huge estates from

estate taxes at very little cost.

The outlay for $200 million of insurance at average age 80 is about $66 million

and the gift taxes due on the transfer are about $36 million. $36 million left in

the estate is reduced by estate taxes to about $16 million so now it is only $16

million which effectively exempts $363 million from estate taxes. Even at such an

advanced age, still a highly optimized program.

You can customize this program to achieve fantastic results for an estate of virtually

any size up to $363 million. It is only on sums in excess of $363 million that any

complicated estate planning is justified.

TURN ANY TAX INTO AN ASSET

There is almost certainly no greater expense that your estate will ever face than

the inevitable expense of estate taxes that can claim up to 55% of everything you

own.

Legal documents can shelter some of your assets and you are wise to give away your

full allotted tax exempt gifts each year. But still, whatever is left in your estate

to provide for your lifestyle at the time of your death will be subject to the very

expensive expense of estate taxes.

It doesn't have to be that way.

Using Wilson Financial pioneering techniques, you can turn your estate tax expense

into a highly optimized asset for your heirs.

Let's say you have $3 million left in your estate after all planning has been undertaken.

Remember you can pro rata all figures in this example up or down as needed to fit

your individual situation. Estate taxes on that $3 million will be $1.1 million

leaving only $1.9 million for your heirs.

But what if you 'spent' the $1.1 million now? It's lost money. Forfeit to the tax

man if you die with it in your possession.

You could just give it to your heirs now. That would reduce your estate to $1.9

million, below the level where estate taxes are levied. And, using both you and

your spouse's combined $1.2 million Unified Gift and Estate Tax Exemptions, you

would not have to pay any tax on the transfer.

But there is a much better way to go. A means to optimize your inevitable tax expense

into a significant asset.

If you were to take the $1.1 million out of your estate now and use it to purchase

a last-to-die life insurance policy on the lives of you and your spouse, you could

receive a return of 10-to-1 if you are average age 60; 5-to-1 if you are average

age 70; and 3-to-1 if you are average age 80. That means your $1.1 million tax expense

can be optimized to be worth between $3.3 million and $11 million, based on current

assumptions.

If your estate is worth $10 million and the tax will be about $5 million, you could

use that $5 million of forfeited tax money to purchase $15 million, $25 million

or up to $50 million of life insurance. Now you must agree that the $5 million is

no longer a tax expense. It is a highly optimized asset producing a significant

return.

Perhaps you are thinking that, left in your estate during your lifetime, the $5

million can be invested in traditional growth vehicles and that the profit it reaps

will recover the tax loss for you heirs.

But consider this: any stock or other investment you bought with the $5 million

would have to grow to $100 million to produce for your heirs the same $50 million

after taxes that the life insurance will provide if you are average age 60, based

on current assumptions. And, to really be fairly compared with life insurance, it

would have to grow to that $100 million tomorrow to be available immediately should

disaster require it.

Can you really think of a single investment vehicle which can produce that kind

of return that quickly? Of course not. But life insurance and ONLY life insurance

can. And that should make the choice easy for you.

MAKING EVERY DOLLAR COUNT - TWICE!

All of the life insurance concepts presented here are based on the ideas of optimizing

and maximizing your funds. Too often, the big picture is not fully considered and

financial losses occur or opportunities are not realized to their fullest extent.

Simple awareness of all the nuances of diversification and planning can avoid the

damage and make every dollar count -- twice. What is meant by making it count twice?

First of all, it is a reference to the consequences of poor estate tax planning.

Allowing your estate to be depleted by up to 55% of its full net worth virtually

halves each dollar you have amassed. By avoiding that depletion, you effectively

make your money worth twice the value it would otherwise have had. Secondly, as

you will see in this example, by reassessing your options and reallocating some

of your funds, you can take a singular financial situation and more than double

the result it yields. That's making your money work twice!

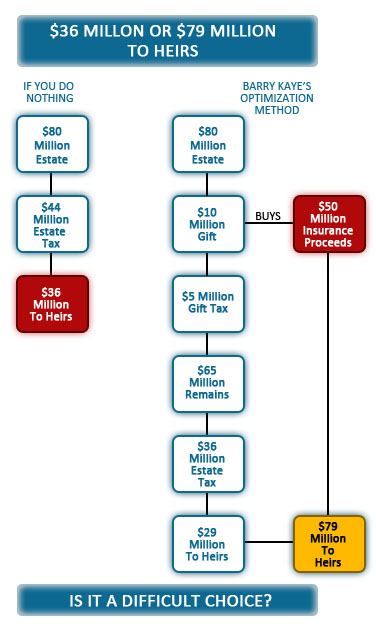

Consider this: you have an estate worth $80 million that provides extremely well

for the needs of you and your spouse and leaves significant principal and interest

not required to maintain your lifestyle. The earnings are just going back into the

overall estate balance.

When you die and your estate passes on to the heirs you have amassed it for, they

will be faced with an estate tax bill for 55% of your estate's total valuation --

$44 million. Your children will be left with $36 million.

But think of this: Since you have more money than you need to support your lifestyle,

you could transfer $10 million to an Irrevocable Trust on behalf on your children.

Though you would have to pay gift taxes of approximately $5 million on the transfer

it is a mere fraction of the $44 million in estate taxes your heirs would have to

pay.

You use the $10 million which you transferred to the Irrevocable Trust to purchase

an insurance policy which, at your combined ages of 70 nets a 5 - 1 return yielding

$50 million for your heirs, income and estate tax free. The $10 million can not

be considered to be an expense or cost since it netted $50 million. So the only

cost involved was the $5 million of gift taxes.

In effect, $5 million netted $50 million for your heirs.

Meanwhile, in actuality, the cost was not even $5 million. If you do not implement

this Investment Alternative technique and therefore are not faced with the $5 million

gift tax, that $5 million will remain in your estate and, as it passes to your heirs,

be reduced by taxes to less than $2.5 million. So it isn't really a net cost of

$5 million to implement this program but $2.5 million.

And it doesn't stop there. The transfer of the $10 million and the gift tax expense

of the $5 million have reduced your estate from $80 million to $65 million which

reduces the estate taxes from $44 million to about $36 million. Instead of $36 million

remaining from $80 million, your heirs now have $29 million remaining from $65 million.

A gain of $7 million.

Had you not undertaken this program your $80 million estate would have been reduced

to $36 million for your heirs. Now, they receive $29 million from your estate after

all estate taxes have been paid PLUS the $50 million return from your insurance

'gain' for a total of $79 million and that is more than double what they would have

received otherwise. THAT is making your money work twice! Why would you pay $44

million in estate taxes and leave your heirs $36 million when you can pay $5 million,

effectively $2.5 million net after taxes, in gift taxes and leave them $79 million?

CREATIVE CONCEPTS

The plans and methods which are presented here depict the amazing variety of usages

to which life insurance can be put to increase your assets, protect your estate,

effectively discount your estate taxes, dramatically increase endowments to your

favorite charity, and more.

In just about each and every case, the simple fact is that no other means exists

to as effectively accomplish the same financial feats. Only life insurance in an

Irrevocable Trust has the exact needed attributes to maximize these concepts. See

for yourself.

CONCEPTS FOR FINANCIAL OPTIMIZING

Many investments are, quite frankly, a gamble. You risk the outcome and hope for

the best. But life insurance is guaranteed to pay at death, based on the assumptions

of interest, earnings and mortality current at the time you purchase it. And, since

its return is predetermined based upon those same assumptions, it can be used in

ways investments couldn't be.

Planning for financial optimization becomes much more clear and direct when the

outcome is known and available at its full value the very day it is purchased. In

a diversified portfolio designed to enhance the value of an estate, life insurance

can achieve unprecedented results of capital optimizing and financial planning.

The examples shown here use life insurance to create and preserve wealth. They are

only a small sample of the myriad ways this amazing vehicle can be integrated into

your portfolio to add a new dimension of options and possibilities. Your own specific

situation will undoubtedly suggest many other ways of customizing these methods

to best serve your own needs.

Select the concepts for financial optimization of particular interest to you from

among the ten listed on the table of the contents to the left.

CONCEPTS FOR ESTATE TAX COST DISCOUNTING

Estate taxes can claim as much as 55% of your estate. If you spent a lifetime amassing

a legacy for your children or favorite charity, they could lose more than half your

total assets to the IRS.

But it doesn't have to be this way. Using the amazing power of life insurance, you

can effectively discount your estate tax costs by a full 90% -- without taking a

single dime away from the government and country that made your wealth possible.

You can even increase your exemptions to the point where you have virtually no tax

exposure at all.

The plans demonstrated here that allow you to accomplish these goals are real. They

are legal. But they cannot be achieved utilizing investments or legal documents

alone. Only life insurance properly structured in an Irrevocable Trust or owned

by your heirs can accomplish the optimization of your legacy to your loved ones.

Select the concepts for estate tax discounting of particular interest to you from

among the six listed on the table of the contents to the left.

13 WAYS TO PROVE LIFE INSURANCE IS NOT AN EXPENSE

Buy Now. Pay Later.

You are over 60 years old. You are worth $2 million or more. You want to buy life

insurance to discount your estate taxes or just to optimize your assets. You want

to increase manyfold what you leave to your children, grandchildren, other heirs,

favorite charity or foundation. BUT -- You do not want to impair your own cash flow.

You do not want to pay now. You would like to make any later payments at your death

and you would like to make the principal and interest tax deductible. You don't

want the expense of life insurance. What do you do?

Conventional wisdom says you can pay for your life insurance on a monthly, annual,

limited pay or one pay basis. The shorter the pay period, the lower the overall

cost, but the greater the short-term cash flow impairment. If you pay annually over

your lifetime there will be a higher total cost but the least annual cash flow impairment

allowing you to buy even more insurance. Also, paying the lower annual premium can

be the cheapest method depending on when you die. Remember that any premiums paid

would have only been worth one half had the money been left in your estate. Then

compare that to the millions this method creates.

More importantly, is there really any cost? Why is life insurance at this age and

with the above stated assets considered an expense?

If you put $1 million into real estate or stocks with the promise that it would

produce $10 million tax free at your death, would that be considered an expense?

ABSOLUTELY NOT!

Then how can you consider the same $1 million put into life insurance that produces

$10 million as an expense?

It's funny how common sense and logic are rarely applied to life insurance particularly

when you realize stock or real estate may not be worth $10 million whenever you

die but insurance always will be (based on current assumptions.)

The answer to not paying premiums is simple. BORROW THE PREMIUM.

Just like you financed your receivables and mortgaged your real estate to build

your fortune, you can borrow the funds to finance your insurance and then either

pay the interest yearly or accrue it until your death. Since the loan, both principal

and interest, is considered a liability it will reduce your gross estate thus reducing

your estate tax.

Uncle Sam will have paid 55% of your debt at your death thus effectively making

the entire loan tax deductible.

You can do this with your margin account at your stockbroker or your bank with low

cost Libor rates. There is also a way to do it with an insurance company but it

may not provide the lowest cost. There are other creative methods of buying insurance

without impairing your cash flow.

You can use your Pension or IRA money if you do not need a part or all of it for

your retirement. Since it will be only worth less than thirty cents on the dollar

at your death after taxes it doesn't make sense to accumulate money here for your

heirs. You don't even have to touch the principal if you freeze your IRA and just

use the yearly appreciation to pay for the insurance. This can effectively increase

your IRA up to 20 times tax-free.

If you are older you can increase your income substantially from Muni's, CD's and

T-bills by purchasing an Immediate Annuity and using the increased income to pay

for the insurance. It can be even more interesting if you borrow the money to buy

the Immediate Annuity. The greater return will not only pay for the life insurance

but can also be enough to pay the interest on the loan.

You can possibly increase your insurance at no cost by reviewing your existing insurance.

In many instances older policies have become antiquated and should be replaced if

you are more concerned with the ultimate death benefit rather than the cash value.

Using the current premium, the existing cash value and a different type policy will

usually make a huge difference.

Also, consider converting an existing annuity into a life insurance policy if you

no longer need the ultimate proceeds for yourself and wish to leave it to your heirs.

This can increase the Annuity proceeds up to 20 times on a tax-free basis with no

additional outlay on your part.

The last five ideas can use either your own money or borrowed money to fund the

policy purchase. However these techniques represent the optimum method of leveraging

your assets for giving to charity at no cost or for your heirs.

You are allowed to gift $10,000 yearly tax free to each of your children. Insurance

can leverage that $10,000 up to $1 million.

You can also gift $600,000 (increasing to $1 million over the next 9 years) without

any gift or transfer tax liability.

Using life insurance, you can leverage that figure up to $20 million tax-free

cash or effectively increase your exemptions up to $40 million.

Turn any tax into an asset for your heirs. Instead of paying $1.1 million tax on

a $3 million estate and receiving nothing back, give the $1.1 million to an insurance

company before you die and your heirs will receive up to $11 million tax-free. This

will pay the tax and leave up to $10 million for your children and grandchildren.

If your estate is $10 million with a $5 million tax due, the same $5 million paid

to an insurance company will pay the tax and leave up to $35 million to your heirs.

This can also be paid for on an annual basis.

Use It or Lose It. If you are worth between $10 million and $20 million you effectively

have no $600,000 exemption unless you use it during your lifetime. You can gift

the $600,000 now and buy insurance and create up to $11 million tax free versus

0.

Finally, here is the most exciting concept for those interested in giving substantial

money to charity at no cost.

Borrow against your portfolio of stocks and bonds, donate money to your own charitable

foundation or favorite charity to buy a life insurance policy with a death benefit

of up to 10 times the amount of your loan. Take the tax deduction and buy a large

policy on your lives for your children to offset the loan at your death. They will

have money left over, your charity will profit handsomely.

You will have paid no money out of your pocket whatsoever and there will be

no cost to your heirs.

The bottom line is you will have bought life insurance and never paid a penny for

it. Good estate planning pays the tax for you, optimizes your assets and never hurts

any other American.

TAKING THE FEAR OUT OF "BASED ON CURRENT ASSUMPTIONS"

It is inarguable that life insurance, performing as a means of wealth creation

and preservation, is the single most reliable and effective estate planning tool

for people who want to optimize their assets and discount their estate tax cost.

Yet many people still resist life insurance because of the phrase "Based On

Current Assumptions" which disclaims all the quotes and proposals they receive.The

caveat carries with it doom-and-gloom ideas of exploding premiums and vanishing

benefits.

However the real tragedy occurs when someone is dissuaded from buying needed insurance

because they do not fully understand the truth of those four fear-provoking words.

And it is made worse by attorneys and accountants who are not knowedgable on the

subject and who manipulate people's fears to convince them not to buy. Even some

unscrupulous insurance agents will intentionally misrepresent the facts about the

impact of "based on current assumptions" on a competitor's proposal just

to steal the business.

What exactly does "Based On Current Assumptions" mean? How does it

impact a policy's cost and return?

These are important things to know and understand before buying a life insurance

policy.

The return on a life insurance policy is calculated by the insurance company based

on your expected mortality (how long you can be statistically assumed to live given

your age and current health) and the interest rates they are currently earning on

the money you pay them. It is how those earnings go to their bottom line of expenses

that dictates their profit.

When you apply for a policy, you are quoted a price that will yield a quoted return

"Based On Current Assumptions."

As long as the mortality assumptions made about the group you fall into and the

interest rates the insurance company is earning on your money hold to current levels,

you will receive the death benefit that was presented to you for the cost that was

quoted. Even given the limits implied by the caveat, this is still far more of a

certainty than you could expect from virtually any investment.

Let's look at the factors upon which "Based On Current Assumptions" rests.

First, mortality. The longer you live, the more premiums the insurance company collects

and earns returns on. Therefore, the less your policy costs.

It is not changes in YOUR mortality expectations that can effect the cost of

an insurance policy.

It is changes in the mortality assumptions of the whole pool of potential insureds,

basically the population of America, in most cases. And those mortality assumptions

have improved for many years.

However, the insurance company must show the maximum mortality charge that is reflected

as a major part of the guaranteed column of your policy proposal in accordance with

legal requirements even though the potential of mortality assumptions reversing

and going to their maximum (which is used to protect the client by putting in a

ceiling) are remote.

The other major aspect of the assumptions is based on interest earnings. Remember,

the more interest the insurance company can be expected to earn with your money,

the less the cost for your desired return. If interest rates go up, allowing the

insurance company to realize higher yields on their investments, the cost of the

return you want goes down. If interest rates go down, causing the insurance company

to earn less with the same money, the premium to produce the originally determined

amount of death benefit, goes up.

But you must remember that the horror stories you've heard of hugely ballooning

premiums were caused by policies years ago when interest was 10% to 12%. Right now

we are living in a world of approximately 6% to 7% interest. The guarantee in almost

all policies is no less than 4%. From 11% to 4% was a huge drop that necessitated

large premium increases. But from our current 6% to 7% the worst potential scenario

doesn't make such a big difference. Let's take an honest look at what could happen.

Based on current assumptions the yearly cost for a $1 million last-to-die policy

purchased at average age 60 on a life-pay basis is approximately $7,551. If interest

assumptions go down 1% the yearly cost rises to $8,691.

Clearly, the increased cost is minimal and, when measured against the return, its

tax free nature and the fact of its immediate availability, almost negligible in

relationship to the resulting death benefit.

Now, let's look at it the other way. What if interest rates go up as I think they

are much more likely to do.

The same policy currently costing $7,551 annually would only cost $6,288 a year

if interest rates go up 1%. The difference can be used to fund additional premiums

or can save yearly cash outlay. In either event, the policy still produces the same

$1 million.

When you really think about it, you will realize that all your investments, with

the exception of some very conservative, safe but low-yielding bonds, are interest

sensitive and based on current assumptions. Our whole economy is. There is nothing

so different or so fearful about the investment alternative of life insurance.

Your stocks offer you NO GUARANTEE at all. Your real estate offers you NO GUARANTEE

at all. Your CD's and savings account are completely dependent upon the current

interest rates exactly as a life insurance policy is. Yet, none of them can perform

as well as a life insurance policy can for the ultimate good of your family whether

their need of it comes tomorrow, in one year or twenty years from now.

Even with the caveat of current assumptions, interest is guaranteed never to be

lower than 4% depending on the individual company. And if interest or mortality

changes, you can always pay more, reduce the death benefit or do nothing if you

still think the policy will last longer than you will.

Furthermore, many companies have now introduced guaranteed policies. You pay more

for the security of never having your premiums change but for some people it is

worth it.

Personally, I recommend going in at the lowest rate possible. You can always make

up the guarantee and interest later if the need arises. And what is the point of

spending money needlessly now in anticipation of a worst case scenario that may

very well never come? Especially when you can always deal with it later if you have

to.

The bottom line is nowhere near as baffling as it may have seemed before. Given

the interest and mortality assumptions being utilized to determine policy returns

today, it is my opinion that there is no better time for consumers to benefit from

the many financial opportunities afforded by a properly structured life insurance

policy used as part of a diversified financial portfolio.

WHO SAID YOUR LIFE INSURANCE CAN'T BE GUARANTEED?

People, in my experience, like to find reasons not to believe in the power of

life insurance.

I have never fully understood why they would desire to deny something so uniquely

beneficial and inarguably effective, but they do.

Sometimes the denial occurs on the part of attorneys or advisors. This could lead

to the filing of malpractice lawsuits. Other times, it is based on a general dislike

for the industry or an unfortunate experience with an over-zealous or unscrupulous

salesperson.

Mostly, I believe, the prejudice simply stems from a desire to disassociate from

the unrelenting fact of our own mortality. I find this terribly ironic, in much

the same sad way that a fear of a bad diagnosis often keeps people from going to

the doctor until they have put it off so long that they wind up fulfilling their

own dire expectancy. The condition which could have been treated and healed is too

far gone and there's nothing more to be done. The metaphor applies to life insurance

and estate planning in the same way.

But few people admit that their reluctance is based on their own fears or perceptions.

Instead, they seek to discredit the products and programs to justify their misgivings.

The most common of these justifications that I hear has to do with the fact that

the cost of life insurance policies is variable. That, because the premium amounts

are based on current assumptions and could change as interest rates and mortality

statistics changed, they might blow up or the benefits might vanish.

It was never a particularly valid argument. Costs and returns are rarely guaranteed

for any financial vehicle. Life insurance is far from unique in this. Moreover,

given the current interest rates, the likelihood of change is, in my opinion, to

the benefit of someone buying a policy now. I don't think interest rates are going

to go down any further but I do think they could go up based on future inflation.

And if they do, the cost required to produce your needed death benefit will go down.

Which means that either your rates will go down or the same amount of money will

buy more coverage.

Still, people would look at me and say, "But you don't know that for sure.

You can't guarantee it." And then they would fail to take the one step that

could protect their heir's legacy better than anything else.

Now when I find myself in that conversation, I let the person raise their objection

and then I say, "Yes I can."

It may be one of the most exciting innovations in the life insurance industry

since the advent of the last-to-die policies. New policies can actually guarantee

their returns irrespective of mortality or interest rates.

There are two ways of structuring policies to provide for these guarantees.

First of all, there are a few companies that are actually writing guaranteed policies.

They do cost a little more. A $10 million policy for a man and woman average age

60 based on current assumptions could be expected to cost about $1 million on a

one-payment basis. That same $10 million bought by the same 60 year old couple on

a guaranteed basis could be expected to cost $1.4 million.

But peace of mind and certainty are valuable commodities well worth a little more

to many people. For them, these new guaranteed policies can make the entire difference

between acceptance or denial of the best programs available for estate tax cost

discounting or ultimate asset optimization.

To give you a basis of comparison, we have always said that, in general and based

on a last -to-die policy on two people with preferred ratings, returns on policies

bought with one payment based on current assumptions could be expected to be 10-to-1

at average age 60, 5-to-1 at average age 70 and 3-to-1 at average age 80. For the

guaranteed policies, those returns change to about 7-to-1 at age 60, 4-to-1 at age

70 and 2-to-1 at age 80.

The other kind of guaranteed policy costs more but it offers absolutely phenomenal

growth opportunities.

By structuring a policy using the extreme calculations of guaranteed minimum

interest and maximum mortality, you can guarantee that your cost for that policy

will never go up or your death benefit down.

But of course, basing the policy on these extremes will drive the premium way up.

For most people, the difference in cost makes the policy both prohibitive and undesirable.

For example, a couple, average age 40, could buy a policy with a $10 million return

for about $26,000 a year based on current assumptions. To guarantee the policy,

it would cost them $94,000 a year.

Why would anyone spend $68,000 more a year for the same return? Well, there may

be some people for whom the peace of mind is worth it who can't qualify for the

less expensive guaranteed policies I mentioned earlier. But it still seems counterproductive,

especially when you consider that the 'extra' $68,000 a year the couple is paying

could produce about $36 million more of death benefit based on current assumptions.

There is however, one amazing benefit to this type of purchase structure.

As you pay premiums significantly in excess of what the current assumptions